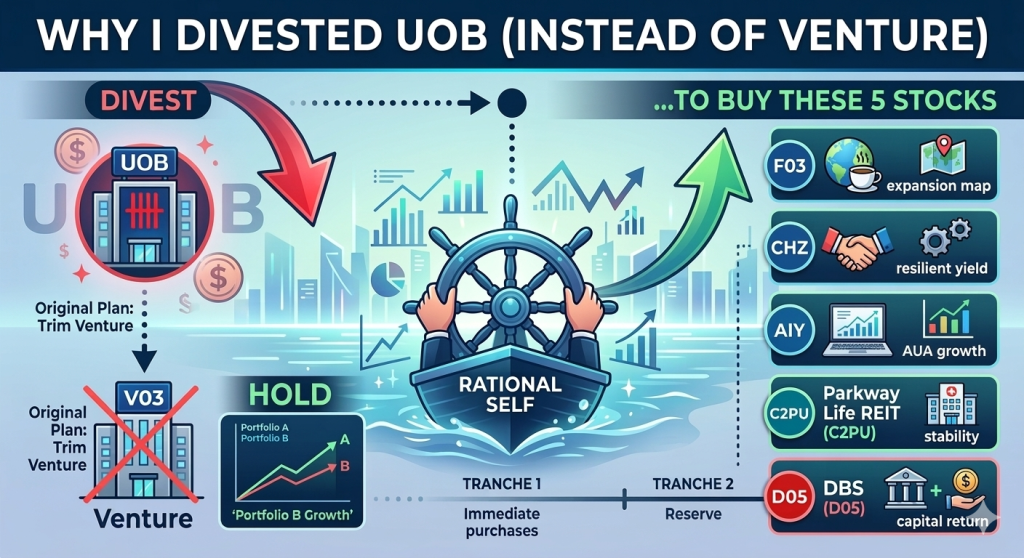

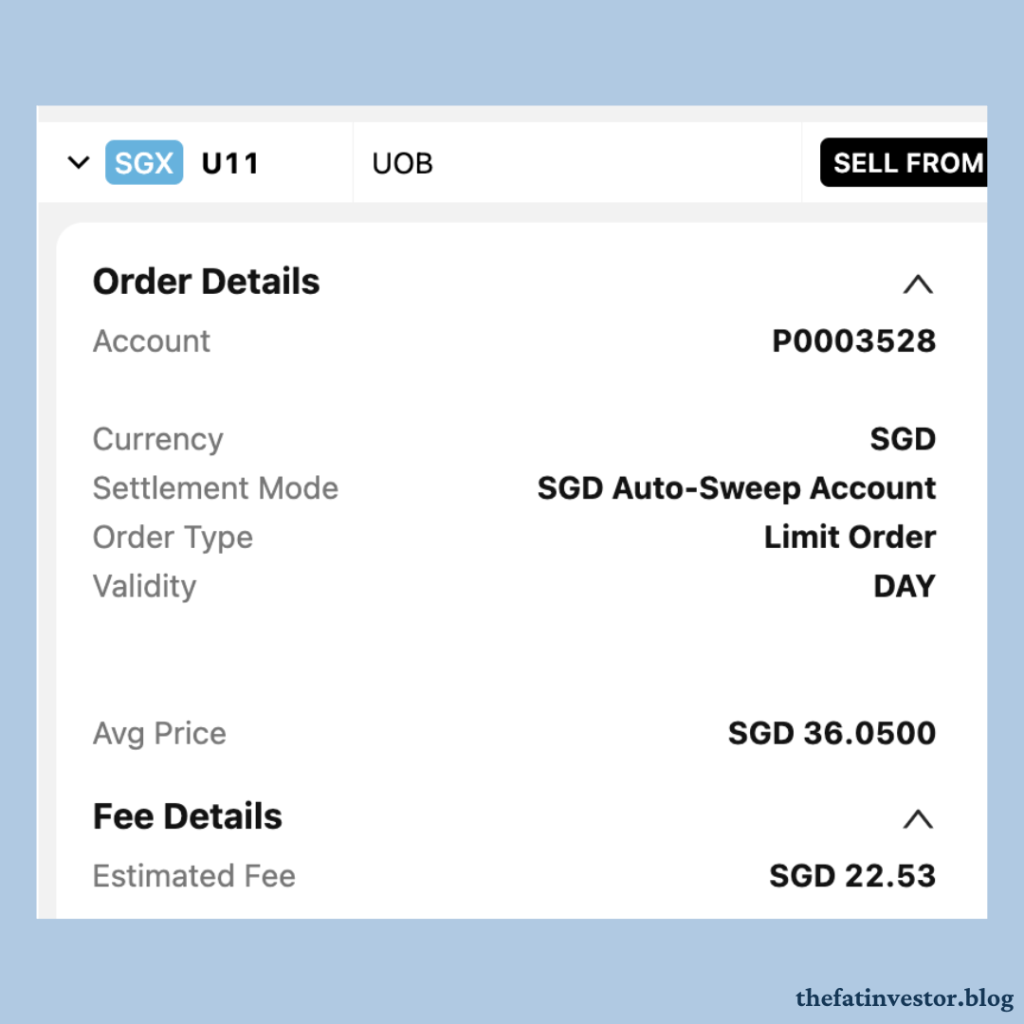

I exited UOB (U11) last week.

While it wasn’t a panic move, the escalation in the Middle East accelerated my decision to swap out of this position to raise funds for my other intended buys.

Interestingly, my original plan was to trim my position in Venture (V03).

The emotional me was disappointed that management didn’t bump the final dividend despite a robust balance sheet. I almost pulled the trigger, but missed a price rebound and paused.

That delay allowed my rational self to take back the wheel. I realised intuitively that a turnaround for Venture is likely around the corner, and when I dove into the data, the trend became clear.

The numbers tell the real story.

Portfolio A (Lifestyle) has finally stabilised, holding flat at S$222 million for the last two quarters of 2025.

Meanwhile, Portfolio B (Networking & Communications) has been growing steadily, climbing from S$375 million in the first quarter to S$424 million by the last.

My simplistic thinking is this: Even if Portfolio A remains soft in the coming months, the momentum of Portfolio B is now large enough to move the needle for the entire group.

You are likely looking at the “inflection point” where the growth engine finally outpaces the unusual decline in the Lifestyle domain due to increased reliability.

Barring further unexpected developments, FY 2026 should be stronger.

Consequently, I see a high probability of this year’s S$0.05 special dividend being converted into a permanent ordinary dividend.

At S$15.41, an S$0.80 total dividend provides an attractive 5.2% yield with significant upside from further growth in Portfolio B.

Why I Divested UOB

With Venture now a “Hold,” the capital had to come from elsewhere.

I looked through my income counters, checked their current yield and assessed their outlook for the next few years.

My eyes fell back onto UOB–the stock I had already trimmed intuitively in late February when DBS (D05) reported a weaker fourth quarter.

With 4Q profits down 7% and the final dividend cut from S$0.92 to S$0.71, the stock’s 2% YTD resilience felt like an exit opportunity rather than a reason to stay.

Even using a 1H 2025 interim dividend (S$0.85) as a guide, an S$1.70 dividend in FY 2026 provides a forward yield of only ~4.7%.

While decent, in this environment, there are better offers with higher yields and superior growth potential. I’m grateful for the 45% total return UOB delivered over the past three years, but it’s time to redeploy that capital where it can work harder.

My Reallocation Plan: What and When

The original intent was to trim Venture, one of my larger holdings, to increase my stakes in Food Empire (F03) and HRnetGroup (CHZ)

However, the full divestment of UOB has provided a larger capital pool. Combined with the spike in market volatility, I’ve adjusted my plan to balance aggressive growth with rock-solid stability.

What I Intend to Buy

Here is a brief look at why these stocks are back on my radar. For a deeper dive, you can refer to my previous analysis posts linked at the end.

- Food Empire (F03): The growth pipeline is clear. Expansion in Kazakhstan, Malaysia, India, and Vietnam is moving from “plan” to “execution.” If they continue to execute, we are looking at a significantly larger business five years from now, which should translate to both capital gains and increasing dividends.

- HRnetGroup (CHZ): With a 5.6% yield and S$263M in net cash, HRnet provides a resilient income stream. It’s a “pay-to-wait” play; I’m happy to collect the dividends while waiting for its organic growth “green shoots” to flourish.

- iFAST (AIY): The twin engines of the HK ePension business and iFAST Global Bank (iGB) are revving up. The recurring nature of their wealth management model—and the unlimited potential of a global digital bank—suggests that the S$100 billion AUA target is a matter of “when,” not “if.”

- Parkway Life REIT (C2PU): In an uncertain market, PLife is a “no-brainer.” The high-visibility 24% rental step-up coming in 2026 offers a level of stability and price re-rating potential that is hard to find elsewhere.

The DBS Decision: Conviction vs. Caution

Finally, I want to talk about DBS (D05). While all three major Singapore banks are fundamentally strong, DBS continues to stand out.

Even as they feel the strain of declining Net Interest Margin (NIM), DBS has managed the transition through loan book growth, strategic hedging, and explosive growth in their Wealth Management segment.

I particularly appreciate the clarity of their management; using an absolute dividend guide (S$0.81 per quarter) rather than a shifting percentage payout offers the kind of predictability a DIY investor needs.

However, I share the common concern: Can DBS sustain the S$3.24 annual payout (S$2.64 ordinary + S$0.60 capital return) after FY 2027?

To be honest, I am still deliberating.

The core question is whether they can grow Non-Interest Income (Non-II) fast enough to replace the inevitable decline in NII once interest rates settle, all while keeping the payout ratio around 70%.

I don’t have a crystal ball, but I believe that among the three local banks, DBS — with its achievable 15% ROE target —is the most likely to successfully convert those “special” dividends into permanent “ordinary” ones.

Therefore, with the recent price dip, I am looking to increase my stake slightly.

When I Intend to Buy

It is impossible to perfectly time the market during a major conflict.

With Brent crude already surging past $90 and the threat of a prolonged blockade in the Strait of Hormuz, the price action for Singapore stocks is likely to remain volatile and switch quickly.

Instead of speculating on the war’s duration or its impact on energy costs, I am deploying my funds in two deliberate tranches.

Tranche 1: The Tactical Entry (Coming Week)

I will deploy a portion of the funds in the coming week.

Despite the noise, I believe the current prices for my picks are sufficiently attractive for my long-term thesis. If the conflict de-escalates faster than expected, this tranche will benefit from the immediate “peace dividend” and market rebound.

Tranche 2: The Defensive Reserve

I will keep the remainder in reserve, to be deployed only if the conflict drags on and causes further structural weakness in the market.

While the rational me knows this could lead to a “better” entry price, the human me hopes this scenario never materializes.

Ultimately, I would rather pay a higher price for my investments if it means the world is a more peaceful place.

Related Posts

My Psychological Buys: “Timing the Market” for Time in the Market

Beyond DPU Jump: Potential 15% Return for Parkway Life REIT in 2026?

iFAST Galloping into the Fire Horse Year. Price Doubling in 5 Years?

Beyond DBS and S-REITs: Food Empire and HRnetGroup Deliver Record Dividends

Disclaimer

This content is for informational only. I am not a financial advisor, tax professional, or legal expert, and the information shared here does not constitute personalised financial advice, nor is it a solicitation to buy or sell any securities or financial instruments.

All opinions and commentary reflect my personal views and are based on general market commentary.

You are solely responsible for your own financial decisions. Investing involves risk, and any action you take based on the information provided on this blog or channel is strictly at your own risk.

Always conduct your own research and due diligence and consult with a qualified, licensed financial professional, tax professional, or legal advisor before making any investment or financial decision.

Discover more from The Fat Investor

Subscribe to get the latest posts sent to your email.