For the last few years, AEM (AWX) and The Trade Desk (TTD) shared one exhausting trait: the struggle.

Both were stocks I watched closely as they navigated macro headwinds, industry cycles, and skeptical sentiment. But the latest round of results has finally broken that bond.

While I’m feeling the “sour” taste of a TTD plunge, the “sweet” surge in AEM masks it.

Honestly? I’m happy with the divergence, much in the same way my palate enjoys a good plate of sweet and sour pork.

The contrast is what makes the overall experience work. It’s a vivid reminder of why we diversify and why, sometimes, patience looks different for every ticker.

TTD: Can It Ever Recover?

After quarters of tepid performance, I didn’t have high expectations for TTD’s 4Q 2025.

It turned out “fine” on the surface, with revenue growing 14% YoY to $847 million, beating consensus. While that is a clear slowdown, it was somewhat expected given the lack of election ad spend this year.

But the 1Q 2026 guidance was the real “sour” note—management is projecting just 10% YOY growth for the coming quarter (approximately US$678 million).

That threw me completely off-guard.

My mental note was that while TTD’s hyper-growth period might be over, it should still comfortably pace at a 17–18% range.

Moreover, I was hoping that once their internal re-organization was complete, they might surprise us by growing above 20% again, causing the stock to be re-rated.

Instead, we got a screeching halt. For a growth stock with this kind of valuation, 10% isn’t just a “lull”—it’s a red flag!

It leaves me asking some uncomfortable questions:

- Is this a “low-ball” target? Jeff Green is known for being conservative, but this feels deeper than just sandbagging expectations to set up a “beat.”

- The Market Share Leak: Have they underestimated Amazon’s (AMZN) aggressive reach into Consumer Packaged Goods (CPG) and automotive segments?

Are newer and hungrier competitors like Zeta Global (ZETA), with its AI-driven marketing automation, chipping away at the “moat” TTD once shared with premium agencies? Zeta’s recent “beat and raise” streak makes TTD’s 10% look even slower. - Ventura’s “Adventure” turning sour? There was a lot of hype around Ventura, but it feels like a complex gamble. They recently pivoted to the “Ventura Ecosystem”, partnering with players like V and Nexxen, which suggests that building a standalone OS was harder than anticipated.

Did they miss the boat by not just striking a simplified deal with a giant like Roku (ROKU)?

I don’t have all the answers yet, but the numbers suggest these aren’t just minor missteps. Between the aggressive push for UID 2.0 and the complex Ventura gamble, it feels like TTD tried to bite off more than the market could chew.

By misreading its own competitive strength in a shrinking ‘Open Internet,’ TTD didn’t just stumble—it missed some major turns while newer, AI-native players like Zeta and retail giants like Amazon were busy taking its lunch.

AEM: The Recovery is Real (and Early)

Now, let’s talk about something much sweeter. If TTD was the dish sent back to the kitchen, AEM is the honey-glazed highlight that saved the meal. The recovery in 2H 2025 was significantly stronger than what I, or the broader market, anticipated.

2H 2025: Breaking the Losing Streak

The numbers for the half-year ended Dec 31, 2025, show a company finally hitting its stride:

- Revenue & Profit: 2H2025 revenue hit S$209.1 million, pushing full-year revenue to S$399.3 million (up 5% YoY). More importantly, net profit for the half-year surged 32% to S$13.9 million.

- Cash is King: With increased earnings and better operational cash flow (S$133.6M for the year), AEM has moved into a net cash position. This allowed them to slash debt by over 80% and resume dividends with a final payout of S$0.013.

For a stock that felt like a “value trap” just a year ago, seeing cash return to the balance sheet is a massive signal of confidence.

FY 2026: From “Bouncing” to “Ramping”

What’s even more encouraging is the optimism for 2026.

AEM isn’t just “bouncing off a bottom”; it feels like the start of a multi-year cycle of strength. Management is guiding for FY2026 revenue between S$460 million and S$510 million.

At the midpoint, that’s over 20% growth—exactly the kind of “re-rating” numbers I was hoping to see from TTD.

This is driven by a fundamental shift:

- The New “Anchor” Customer: AEM’s second AI/HPC customer is ramping up to high-volume manufacturing. Based on visibility, this customer is expected to become AEM’s top revenue contributor in FY2026.

- The Intel (INTC) Catalyst: While diversifying, AEM is still seeing increased orders from its long-standing HPC customer due to surging CPU demand and AI infrastructure upgrades.

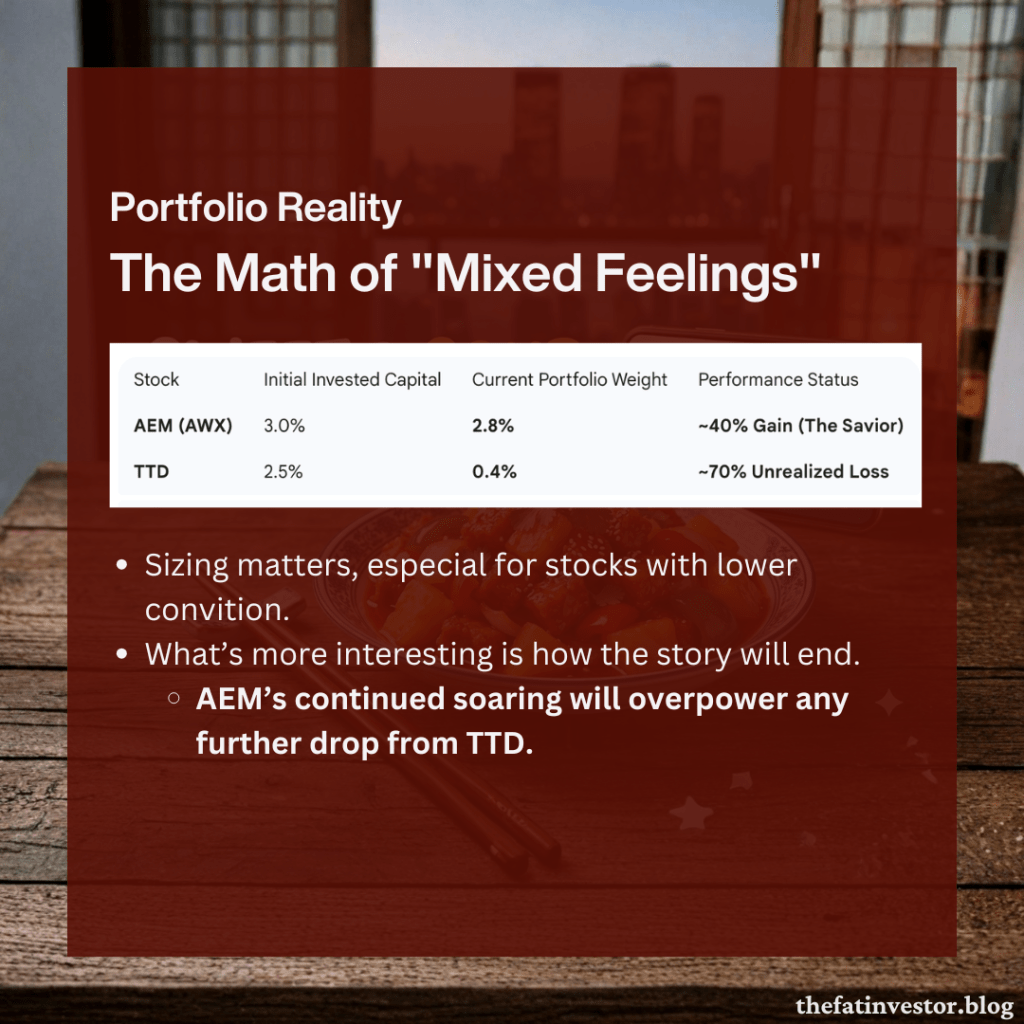

Portfolio Reality: The Math of “Mixed Feelings”

This week is a perfect case study in why position sizing matters, especially for companies where your conviction isn’t absolute.

Based on my initial invested capital, TTD took up 2.5% of my portfolio and AEM 3.0%. Today, the reality is stark: an unrealized loss of more than 70% in TTD is being partially mitigated by a nearly 40% unrealized gain in AEM.

It might appear on the surface that TTD “soured” my AEM investment, but that’s hindsight talking. A year ago, I had no way of knowing which of these companies would recover first.

What’s more interesting is how the story will end from this point forward.

With TTD now whittled down to just 0.4% of my portfolio and AEM sitting at 2.8%, AEM’s continued soaring will completely overpower any further drop from TTD.

It’s a powerful reminder that investing isn’t about being right all the time; it’s about making sure your wins are bigger than your losses over the long term.

My Next Steps

I’m not divesting TTD just yet, though it is now “first in the queue” should I need to reallocate capital elsewhere.

Just as a narrative can change swiftly from positive to negative, today’s laggard can still become tomorrow’s turnaround story.

But for this week? The pork was definitely more sweet than sour.

Disclaimer

This content is for informational only. I am not a financial advisor, tax professional, or legal expert, and the information shared here does not constitute personalised financial advice, nor is it a solicitation to buy or sell any securities or financial instruments.

All opinions and commentary reflect my personal views and are based on general market commentary.

You are solely responsible for your own financial decisions. Investing involves risk, and any action you take based on the information provided on this blog or channel is strictly at your own risk.

Always conduct your own research and due diligence and consult with a qualified, licensed financial professional, tax professional, or legal advisor before making any investment or financial decision.

Discover more from The Fat Investor

Subscribe to get the latest posts sent to your email.