Déjà vu?

Didn’t I ask a similar question in my post last January?

I did.

But this annual ritual isn’t reserved just for Frasers Centrepoint Trust (J69U), or FCT; it’s a mental exercise I perform for every income stock in my portfolio.

It’s my way of verifying that the original thesis still holds and that my capital is working where it should.

Most importantly, it’s a search for potential red flags, so that I’m mentally prepared to act objectively if a “crunch” arrives.

Because FCT’s Annual General Meeting (AGM) is usually the first on the calendar and doesn’t clash with the April/May peak season, it naturally gets the lion’s share of my focus.

Let’s get back to the question: Will FCT finally deliver a meaningful DPU increase in 2026?

To answer the question, we need to look at what’s in store for FCT in FY 2026, and how would these impact its DPU.

Here are my takeaways from the latest annual report and recorded earnings calls, ahead of my attendance at this Friday’s AGM.

(I’ll put up another post if there are any particularly interesting snippets from the floor!)

The Foundation: Consistent Growth Base

There’s no argument that FCT has a very strong portfolio of suburban retail malls.

Their strategic locations — integrated with or adjacent to major MRT stations — ensure consistent, healthy footfall from the surrounding residential catchments.

For FY 2025, this resilience was on full display. Shopper traffic and tenant sales continued their upward trajectory, rising by 1.6% and 3.7% year-on-year (YOY) respectively.

Such robust performance afforded FCT a +7.8% rental reversion in FY 2025. Crucially, even with these higher rents, the portfolio’s average occupancy cost remained healthy at 16.1%.

This meant the tenants’ businesses are thriving enough to absorb the rent hikes comfortably, which is why committed occupancy remained a high 98.1%.

In fact, if you exclude the temporary vacancy from the Cathay Cineplex exit, the portfolio was essentially fully occupied.

There’s no reason to believe this will change in FY 2026. This robust foundation allows FCT to grow steadily through both strategic acquisition and Assets Enhancement Initiatives (AEI).

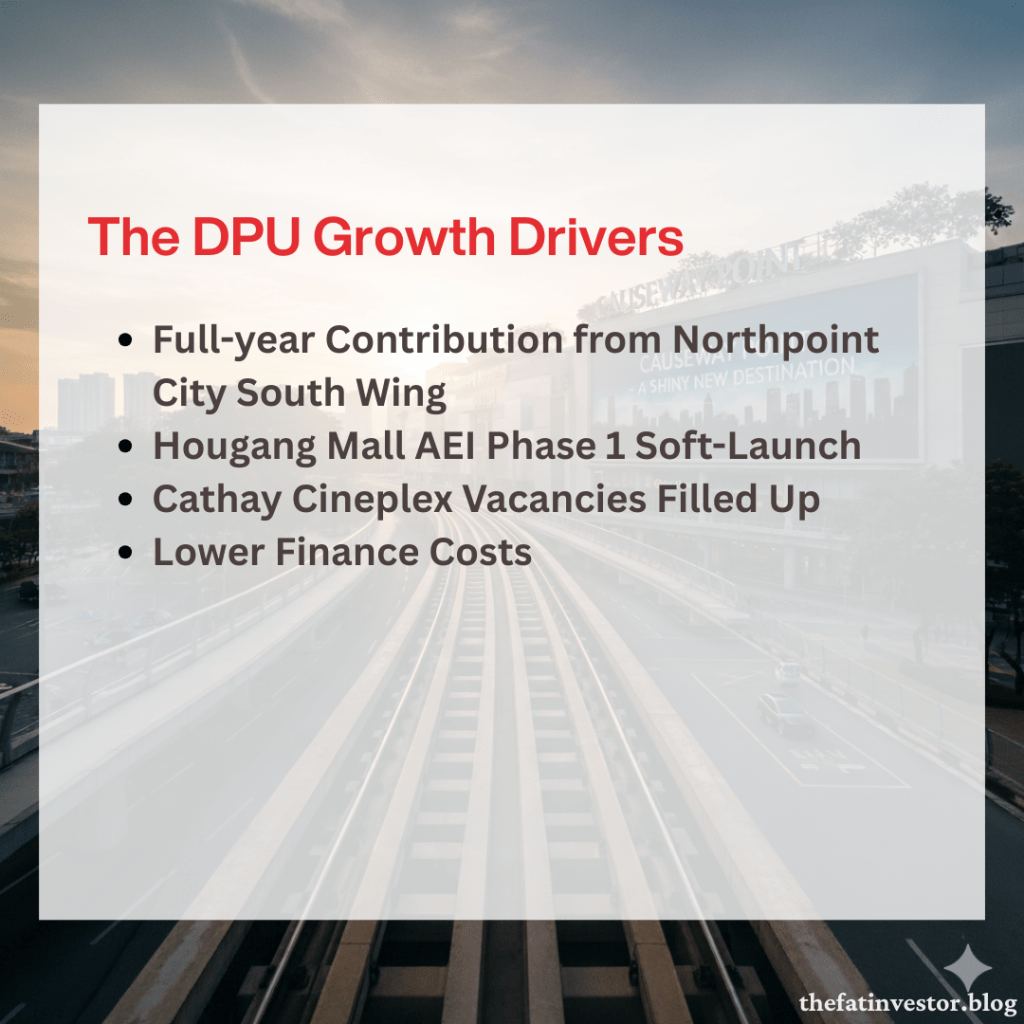

2026 Drivers: From Operation to Finance Costs

With the foundation in place to provide the organic growth, the following factors are likely to boost FCT DPU in FY 2026.

Full-year Contribution from Northpoint City South Wing (NPCSW)

The acquisition was only completed in last May and therefore NPCSW only contributed four months of revenue and Net Property Income (NPI) in the previous financial year, which ended in September.

FY 2026 will be the first time you see a full 12-month contribution from this acquisition, and with the dilution from the share issuance already behind us, the impact would be significant.

In another word, you can add an extra 8 months of income without any further dilution.

Hougang Mall AEI Phase 1 Soft-Launch

The AEI at Hougang Mall is progressing well, with more than 80% of overall AEI spaces have been pre-committed.

While it will take till the end of FY 2026 to complete the AEI, its Basement 1 and Level 1 (which typically has the highest footfall) are opened in January with refreshed spaces.

Given the expected return of investment of 7%, it means there will be a progressive return of “lost” income throughout the year.

Cathay Cineplex Vacancies Filled Up

Part of the reason for the lower increase in DPU for FY 2025 is due to the rental arrears from Cathay Cineplex.

The good news is besides working on the recovery of these arrears, the Manager just shared that it has successfully secured replacement tenants for both the vacated spaces at Causeway Point and Century Square in January 2026.

While the exact tenant list remains under wraps until the 1Q 2026 Business Update, it’s likely that these will be filled up by multiple tenants, resulting in higher yield from these spaces.

It’s unclear how long the reconfiguration will take, but even if it doesn’t contribute to FY 2026, more income will come in FY 2027.

Lower Finance Costs: From Headwind to Tailwind

FCT’s average cost of borrowing has successfully peaked. It declined from 4.0% in 1Q 2025 to 3.5% by 4Q 2025.

With the recent S$400 million green loan secured in early January 2026, there should be further savings from interest payments going forward.

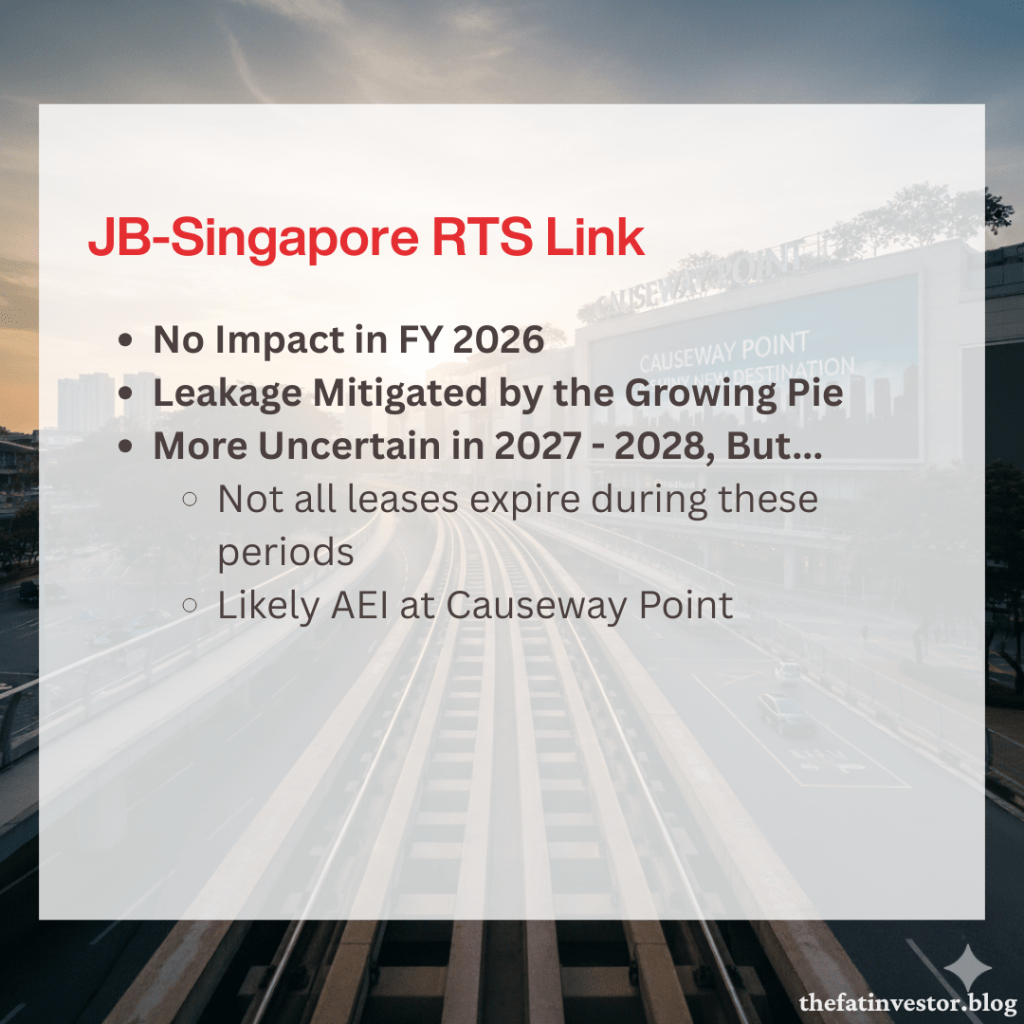

The Elephant in the Room: JB-SG Rapid Transit Link (RTS) Leakage

Since the RTS Link was announced, there’s been a persistent cloud of worry hanging over Northern retail.

The narrative is simple: “Everyone will just hop on a 5-minute train to JB for cheap groceries and dental work.”

Many are already predicting a “Shenzhen-style” exodus that will gut our local malls.

Sensational headlines usually miss the nuance.

For one, JB isn’t Shenzhen; it doesn’t yet offer the same ‘premium-for-less’ experience that draws massive crowds across the border in China.

More importantly, the local spending pool isn’t a ‘zero-sum’ game where a gain for JB is automatically a loss for Singapore; the total pie is actually getting bigger.

Leakage Mitigated by the Growing Pie

According to CBRE’s Retail Property Market Overview (within FCT 2025 Annual Report), the “retail sales leakage” is expected to rise from the current 4% to approximately 5% by 2032.

That isn’t much especially when you consider the massive planned development in the Northern region, such as Woodlands Regional Centre and substantial increase in population from new housings.

To visualise this “Growing Pie” theory, let’s use a hypothetical illustration to see how the math plays out (note: these numbers are for conceptual clarity rather than a direct forecast):

Imagine you own the only bubble tea shop in a small town, selling 1,000 cups a day. Two events happened simultaneously.

- A new road is built and residents can buy cheaper tea in the next town, causing your sales to drop by 10%.

- Your town expanded, and if there’s no leakage in sales you can sell 1,200 cups a day.

The net effect: You can sell 1,080 cups a day (more than before), despite the “leakage”.

The math is clear: a bigger town with a small leak is better than a small town with no leak.

However, the “Growing Pie” theory assumes a steady state. In reality, the developments aren’t concurrent.

RTS Link will be in operation by end of this year, whereas the new housings will only progressively be ready from 2029 onwards.

This timing gap brings us to the “novelty phase” of 2027 and 2028.

The Shorter-Term Impact (2027 and 2028)

While I’m bullish on the long-term math, I’ll be the first to admit that 2027 and 2028 feel a bit uncertain.

When the RTS Link first opens, we should expect a “novelty spike.”

My family is already planning to give it a try. Depending on the experience, we could visit JB a few times a year.

Others might do it more often, hence this might push that “leakage” figure temporarily from 4% to perhaps 6% or even 8% during the first 24 months.

But here is why I’m not losing sleep over my DPU.

- Leases are Shields: Retail leases are generally around three years long with fixed base rents. FCT’s income is structurally insulated from a temporary drop of footfall.

- The Strategic Window for an AEI: There’s indication that Causeway Point is the next major focus for the Manager, with plans already underway to transform it into a regional mall.

This effectively minimises the impact of any temporary footfall volatility by hoarding off sections of the mall when curiosity-driven travel to JB is at its peak.

By the time the RTS hype settles in 2028, Causeway Point would be the “shiny new destination” ready to capture the spending of a much larger Woodlands population.

Conclusion: Will FY 2026 DPU Grow?

The DPU increase in 2025 was a “miserly” 0.6% to S$0.12113.

However, with NPCSW fully integrated, Hougang Mall coming back online, the savings from reduced interest payments, and no impact from RTS yet, the increase for FY 2026 should be noticeably higher.

While not all the gains mentioned above will flow to DPU, as management may retain some cash for potential AEIs at NEX or Causeway Point, I’m hopeful for a 2% to 3% hike.

At the current price of S$2.29, you would be looking at an attractive forward yield of around 5.4%.

I’m holding on to my shares.

Disclaimer

This content is for informational only. I am not a financial advisor, tax professional, or legal expert, and the information shared here does not constitute personalised financial advice, nor is it a solicitation to buy or sell any securities or financial instruments.

All opinions and commentary reflect my personal views and are based on general market commentary.

You are solely responsible for your own financial decisions. Investing involves risk, and any action you take based on the information provided on this blog or channel is strictly at your own risk.

Always conduct your own research and due diligence and consult with a qualified, licensed financial professional, tax professional, or legal advisor before making any investment or financial decision.

Discover more from The Fat Investor

Subscribe to get the latest posts sent to your email.