Love it or hate it, the Central Provident Fund (CPF) is an inescapable pillar of life in Singapore.

While I have my own qualms about its policy shifts and system changes over the years, I remain thankful for having a systematic and safe platform to build towards my retirement.

With the 2025 interest recently credited, my balance is nearly S$1 million across my Ordinary (OA), Special (SA), and Investment (CPFIS) accounts.

Crossing that mark didn’t bring me a sudden surge of joy as I no longer chase specific numbers.

I used to share with my students: consider two people who score 76% and 74% on a Physics test. One gets an A1, the other an A2, but that doesn’t necessary mean the A1 student has a better understanding of Physics.

Grade boundaries are just man-made administrative tools.

In the same way, a “million-dollar balance” is just a benchmark to simplify communication and provide motivation. Whether you are slightly above or below a specific target shouldn’t bother you.

What matters is the system you have built.

I share it primarily to highlight that there are various paths to the same destination.

In the CPF community, the most common advice is to perform manual SA top-ups. While that is a fantastic and effective strategy for many, I chose a different route.

Here is my “winning formation” for the CPF million-dollar game.

Affordable Housing: The Solid Defence

Despite spending hundreds of millions on star-studded attackers like Florian Wirtz and Alexander Isak, Liverpool’s struggles this season often come down to not getting the defence right.

While it takes time for new players to gel and score, a leaky defence resulted in drawing or losing games that should have been won.

In the CPF game, choosing a suburban BTO was my defensive strategy.

Admittedly, it was a bit ulu and lacked immediate amenities. But as a young couple, my spouse and I didn’t mind the trade-off.

In fact, because our mortgage didn’t require a single cent of cash, it gave us the option to afford a small car. It’s made life so much easier, particularly when it comes to getting around with our little one.

By opting for a more affordable home, I ensured that less of my OA was “leaking” out every month to service a mortgage.

I was able to clear my housing loan in just five years, allowing my OA to compound over a much longer period.

I’m not saying it is “wrong” to buy a more expensive flat at a central location or a private condominium. It is a perfectly valid lifestyle choice.

However, it means your CPF will inevitably play a smaller role in your retirement plan unless you have the liquidity to fund those properties with cash.

For my strategy, the BTO was the anchor that allowed the rest of the team to push forward.

Income Growth: The High-Work-Rate Midfield

If housing is the defence, then Active Income is the Midfield.

In any championship-winning team, the midfield dictates the tempo and provides a steady supply of “balls” to the attackers.

Similarly, your salary determines the amount of your CPF contributions and your investable surplus.

It’s simple logic: the stronger your midfield performs, the more “defence-splitting passes” are sent to your strikers.

I was fortunate to be recognised for my contributions early on, but the real breakthrough came when I transitioned into a management role.

That shift significantly boosted my income, but more importantly, I resisted the urge to jump into the property upgrading game.

We could probably afford it.

However, we loved our place and having an aversion to long-term debt, we chose to stay at the same BTO we bought fifteen years ago.

What this meant is every extra ounce of effort from my midfield goes directly toward feeding the strikers: my retirement goals.

Investing: The Prolific Attack

If the Midfield provides the supply, the Striker’s job is to convert that chance into goals.

In my strategy, my CPF investments took this role and accelerated the growth of my capital via the following approach.

1. Exploiting the Long Runway

Because CPF funds are essentially “locked” until age 55, I had the luxury of a long-term horizon. This time-vantage made it much easier to aim for returns exceeding 4%.

However, I remained mindful of the opportunity cost: since the OA has a 2.5% floor, and a transfer to SA yields 4%, my “strikers” had to be clinical.

Most of my chosen stocks (before rebooting my portfolio in 2020) focused on sustainable dividends with yields that comfortably outperformed the SA rate.

2. Active Monitoring vs “Buy and Forget”

A common misconception is treating “Buy and Hold” as “Buy and Forget”.

You are investing in companies that must navigate business uncertainties. And in spite of managements’ best efforts, the ever changing situations could derail their businesses.

My experience with First REIT (SGX: AW9U) and Metro Holdings (SGX: M01) provided valuable lessons. Both were prolific scorers in my early years, but when fundamental red flags appeared, I divested.

Had I not been proactive in “substituting” these off-form players, those gains would have been wiped out.

3. Attacking the Market Dips

Volatility isn’t a threat; it’s an opening.

The long runway gave me the confidence that increasing investments during downturns would pay off.

You don’t always need to pick individual stocks, either.

Utilising ETFs like the SPDR Straits Times Index ETF (SGX: ES3) or the Amundi Index MSCI World Fund is a simple but effective way to capitalise on these situations for the eventual recovery.

The Results

Since merging my portfolios in 2020, I no longer track CPF returns separately, but the numbers speak for themselves.

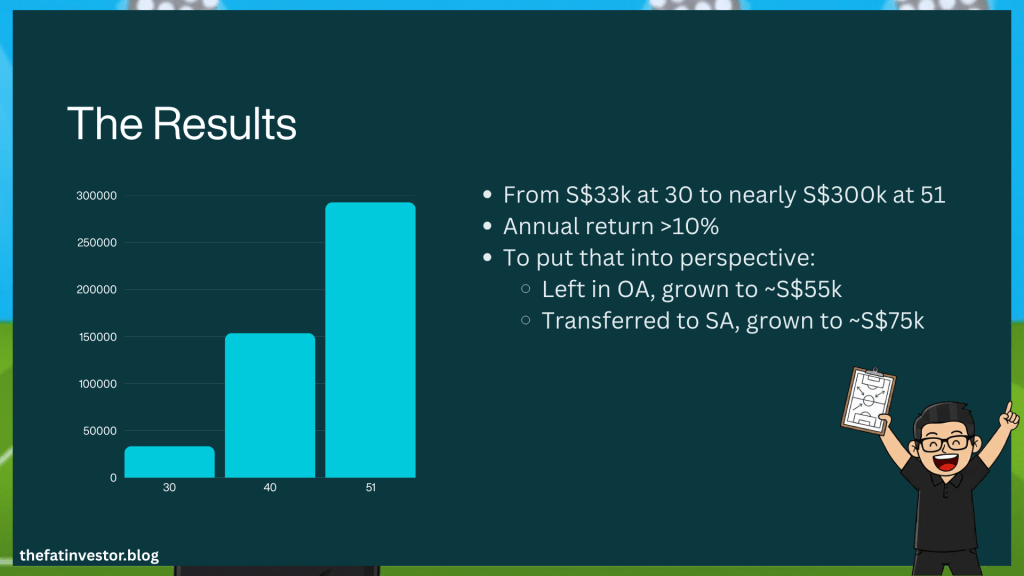

Over two decades, my invested sum ballooned from S$33k to nearly S$300k, indicating an annualised return likely north of 10%.

To put that into perspective:

- Had I left that S$33k in my OA, it would have grown to approximately S$55k.

- Had I transferred it to my SA, it would have reached roughly S$75k.

Finally, because the net amount I’ve drawn from my OA for investment is now negative, it means investment profits alone account for more than one-third of my total CPF balance.

The Long Season

It took you less than 10 minutes to read this article, but hours for me to write it. And the wealth accumulation journey itself took 20 years!

There is no single “wonder goal” or shortcut to this outcome.

It is the result of a coordinated team effort: being prudent with your spending (Defence), increasing your income while preventing lifestyle creep (Midfield), and staying disciplined with your investments (Attack).

Financial success is about staying the course over a long season, even when you hit a rough patch of form.

The best part?

By playing this disciplined strategy, even if you don’t finish top of the table, you’ve guaranteed you won’t be relegated.

Moreover, you will start the next season in a stronger position.

Disclaimer

This content is for informational only. I am not a financial advisor, tax professional, or legal expert, and the information shared here does not constitute personalised financial advice, nor is it a solicitation to buy or sell any securities or financial instruments.

All opinions and commentary reflect my personal views and are based on general market commentary.

You are solely responsible for your own financial decisions. Investing involves risk, and any action you take based on the information provided on this blog or channel is strictly at your own risk.

Always conduct your own research and due diligence and consult with a qualified, licensed financial professional, tax professional, or legal advisor before making any investment or financial decision.

Discover more from The Fat Investor

Subscribe to get the latest posts sent to your email.