Two of my top five holdings, Arista Networks (NYSE: ANET) and Parkway Life REIT(SGX: C2PU), or PLife, reported their 1H 2025 results in the last 24 hours.

These two companies couldn’t be more different, yet they’re the yin and yang of my portfolio.

PLife is a healthcare real estate investment trust (REIT) that invests in a diversified portfolio of hospitals and nursing homes.

On the other hand, Arista is a leading provider of high-performance, software-driven cloud networking solutions for large data centers, cloud computing, and AI environments.

Its increasing market share in the ever-growing demand for networking solutions provides the company a long runway of growth, boosting my portfolio’s long-term appreciation.

The steady and consistent cash flow from PLife, meanwhile, defends my portfolio from market volatility.

Each is strong in its own way, but it’s the combination that makes it potent.

Without Arista, the growth of my portfolio would slow significantly. And without PLife, market volatility could affect my ability to hold onto Arista and benefit from its long-term potential.

Now let’s delve into the key highlights of this quarter’s results.

PLife: Another Quarter of Increasing Dividends

Fundamentally, there isn’t much that I can add on to what I wrote about PLife earlier after attending its AGM.

Its resilient income is driven by:

- Renewed master leases of quality Singapore Hospitals

- Well-managed expansion in Japan’s matured nursing homes industry

- Strategic entry into France’s nursing home market last year

- Prudent capital management and active forex hedging

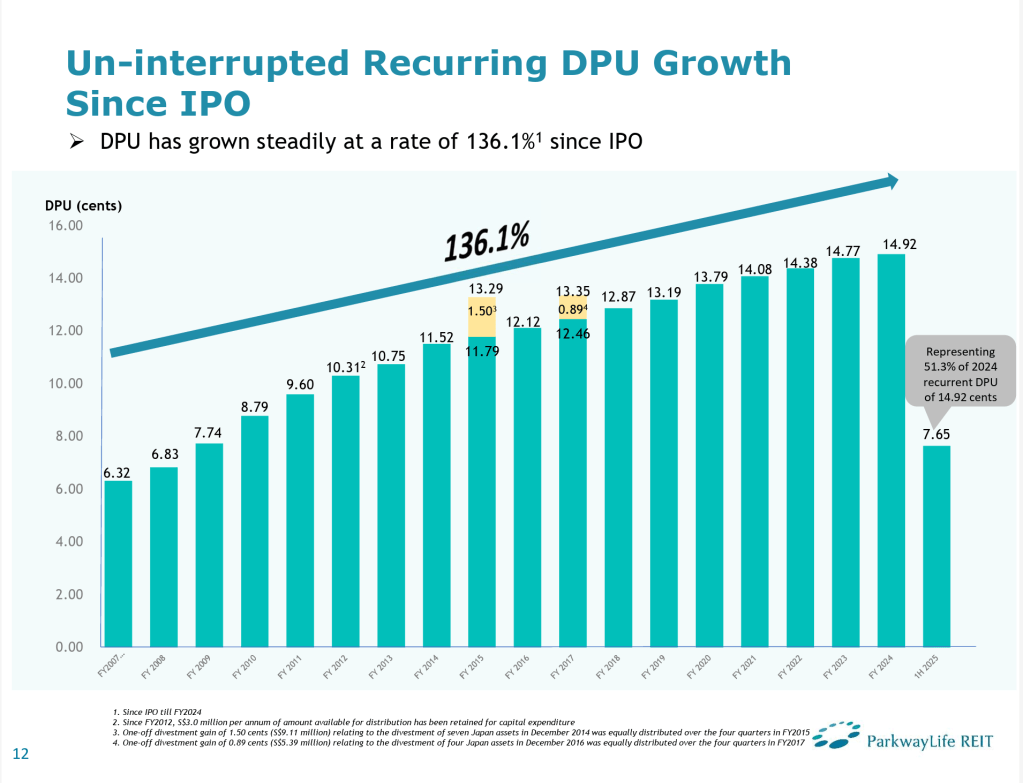

Consequently, dividends per unit (DPU) for 1H 2025 increased by 1.5% year-on-year (YOY) to S$0.0765.

It is likely PLife is able to maintain this level of DPU for the second half, especially with the recent approval from Inland Revenue Authority of Singapore’s (IRAS) of tax exemption for foreign-sourced dividend and interest income from part of its France portfolio.

This tax saving, which approximates S$0.0019 per unit, will provide an additional boost to its recurrent DPU.

Annualising the first half’s DPU and assuming the tax savings is full paid out, the annual DPU will be $0.1549. This translates to a decent forward yield of about 3.8% at current trading price of S$4.08.

Furthermore, DPU is likely to increase further in the next fiscal year, upon the completion of Project Renaissance by the end of this year.

Arista: Riding on the AI Wave

Arista delivered a terrific 2Q 2025 results, with revenue up by 30% YOY to US$2.205 billion, and a 10% increase compared to the first quarter!

Earnings per share (EPS) grew even stronger, nearly 35% YOY to US$0.70.

With this robust performance, Arista raised its full-year guidance from the earlier 17% annual revenue growth to 25%, targeting a full-year revenue of US$8.75 billion.

I’ll admit, the technical specifics of Arista’s business are over my head. But you don’t need a computer science degree to see the company’s clear growth potential.

Their market share is expanding rapidly, and they’re taking a leading role in shaping the future of networking with innovations like Ultra Ethernet.

It is also important to note that Arista’s management is not one to over-promise. In fact, they often over-deliver on their guidance.

For instance, at the last Analyst Day, they were targeting US$10 billion in annual revenue by 2028, but now they are looking to achieve it in 2026, two years ahead of schedule.

Focus on the Long-Term

It’s great to see Arista exceeding its own internal targets.

However, due to the cyclical nature of its business, which depends on infrastructure spending, such exceptional growth does not happen every quarter or even every year.

That said, Arista still has a long growth runway.

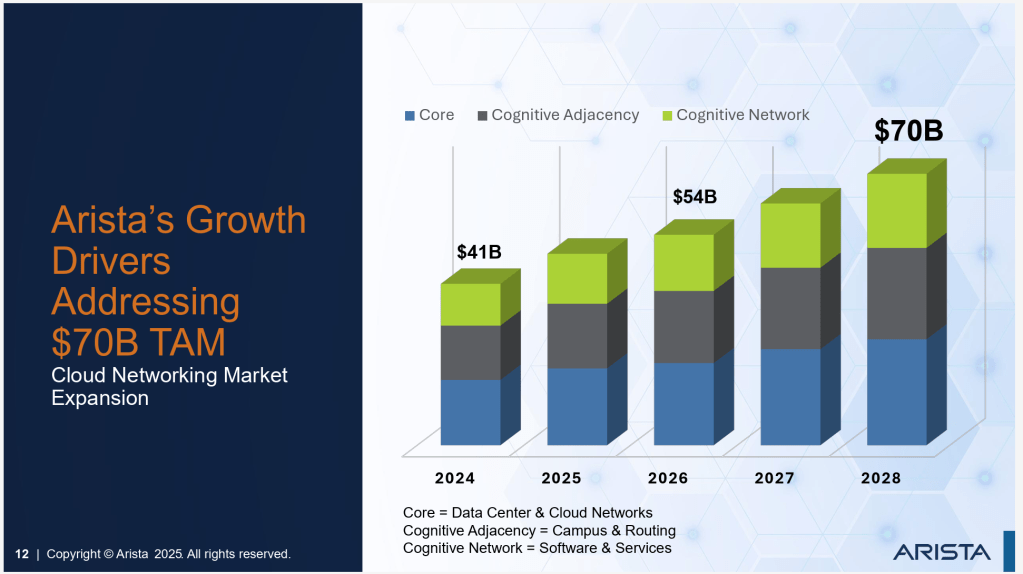

Beyond capturing more market share, the company is regularly exploring new areas to expand its Total Addressable Market (TAM), as evidenced by its recent acquisition of VeloCloud from Broadcom (NASDAQ: AVGO).

This acquisition opens up business opportunities in complementary segments like Software-Defined Wide Area Network (SD-WAN) and Secure Access Service Edge (SASE).

Based on the company’s own estimates, a more sustainable long-term growth rate is in the high teens. This is a respectable pace for a company of Arista’s size and a massive potential when compounded over the long term.

This kind of consistent outperformance is why I’ve been a shareholder for seven years.

Both Arista and PLife are quality businesses, led by strong and competent leaders, and have not disappointed me since my initial investments.

I continue to see their potential for further growth for the next decade, and as such, I will continue to hold onto my current stake.

Help Me Raise Funds for Autism Resource Centre (SG)

I’m participating in this year’s fundraising event: A Very Special Photo Challenge.

A little background on this challenge.

ARC(S) is building and expanding services to support adults with Autism Spectrum Disorder (ASD), addressing their growing needs in areas such as employment, lifelong learning, independent living training, and residential housing.

Funds raised will go towards supporting these vital services to empower them to lead independent and meaningful lives beyond their school years.

If you’ve found value in my writings and insights, please consider donating to this cause by clicking here or scanning the QR code below.

Thank you.

Discover more from The Fat Investor

Subscribe to get the latest posts sent to your email.