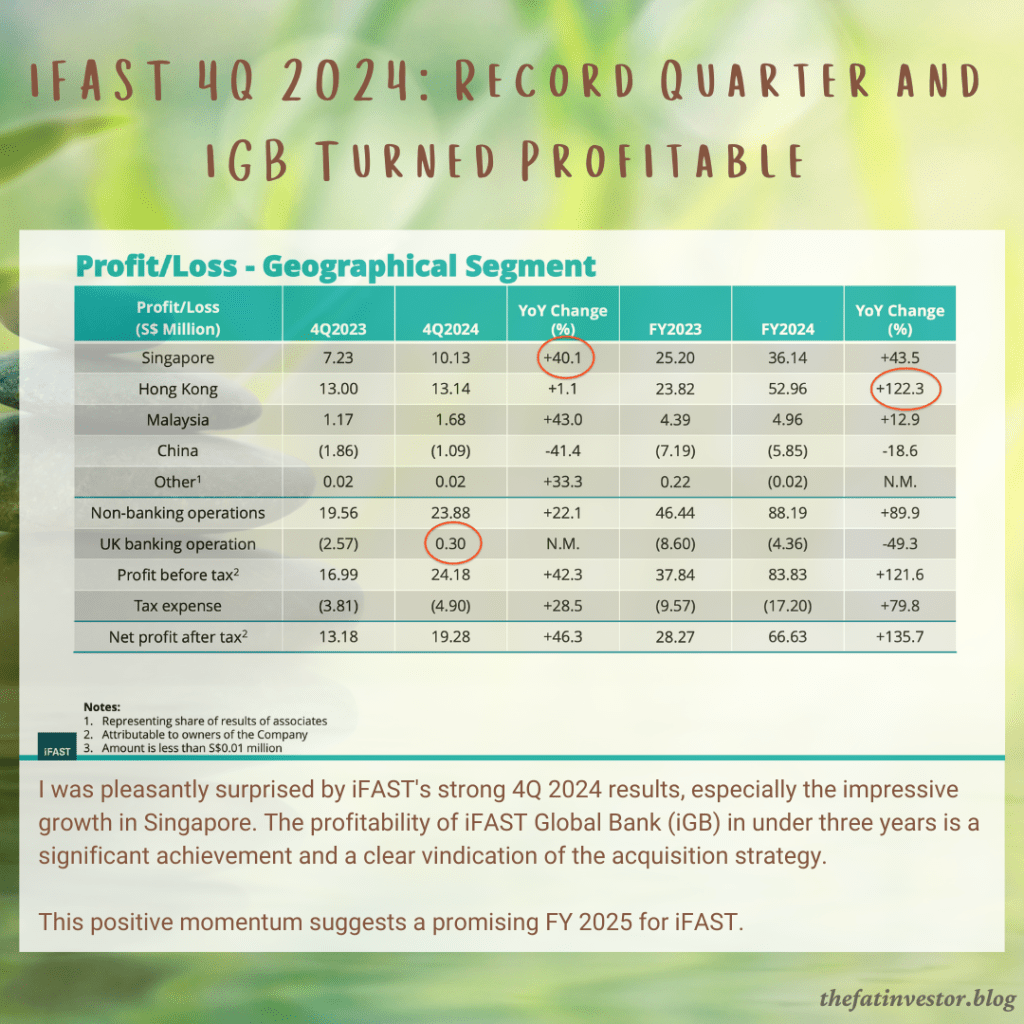

iFAST Corporation (SGX: AIY) delivered another record quarter. While growth moderated in 4Q 2024 as anticipated, the 46% year-on-year increase in net profit to S$19.28 million significantly exceeded my 30% projection.

Several factors contributed to this strong performance. Beyond the expected contribution from the Hong Kong (HK) ePension division, I was particularly pleased with the robust growth in the Singapore segment.

Most notably, iFAST Global Bank (iGB) achieved profitability, a significant milestone.

iGB continues its impressive growth trajectory, with customer deposits reaching a record S$1.01 billion, up 25% quarter-on-quarter. This strong deposit growth has fueled accelerating improvement in its bottom line throughout the year.

Continued deposit growth in FY 2025 is expected to drive further net profit expansion for iGB.

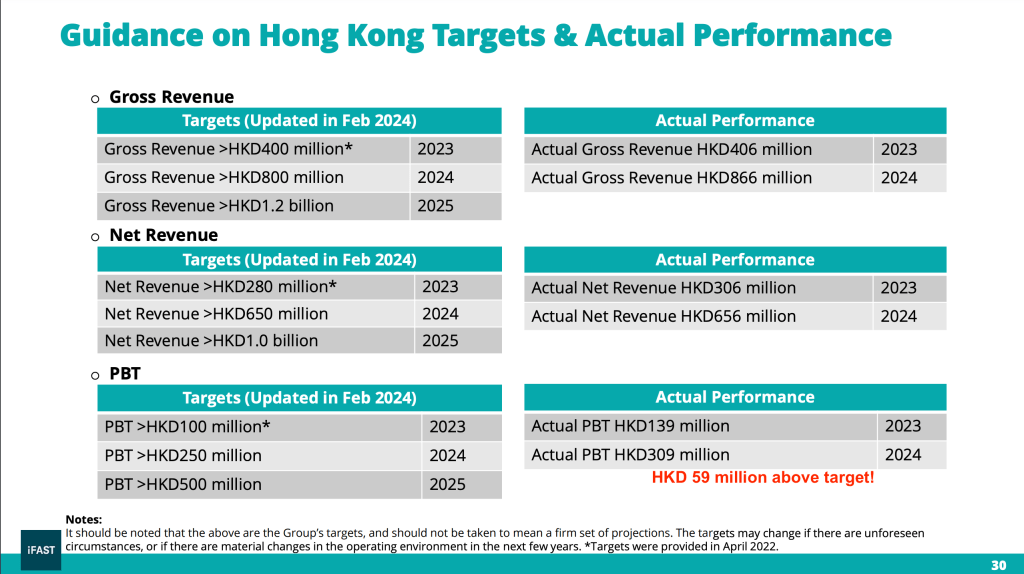

The HK segment also continued its strong performance, exceeding the target set in 2022. Given this track record and ongoing momentum, I am confident that the segment will surpass its targeted profit before tax (PBT) of HK$500 million next year.

The upcoming launch of the ORSO platform in 2Q 2025 and potential collaboration for its Macau pension business further strengthen the outlook for this segment.

Based on these positive developments, and barring unforeseen circumstances, I project earnings per share (EPS) of over S$0.35 for FY 2025, a near 60% increase from this year’s S$0.2239.

At yesterday’s closing price of S$7.64, this translates to a forward price-to-earnings (P/E) ratio of approximately 21x, an attractive valuation given its growth prospect.

Additional notes after attending the earnings call

1. NII will continue to increase next year with increased deposits (looking to double it next year) and possibly increased NIM. Unlike other banks, iFAST gave its customers higher rate. As they develop and grow the services, they aim to have higher NIM.

2. The potential collaboration of Macau pension business will be similar to ORSO which will contribute to the group’s AUA. No material impact for FY 2025.

3. While there will be further increase in OPEX next year, the ratio to revenue should not deteriorate. PBT should be able to maintain or improve from current level.

Discover more from The Fat Investor

Subscribe to get the latest posts sent to your email.